Confirm You’re Real!

You’re almost there! We’ve sent you an e-mail to confirm that you’re a real person.

After you confirm we’ll send you the full financial plan in PDF format, plus we’ll give you a quick overview of the highlights within the plan.

Debt Payoff

Michael and Julie have $17,256 in debt from an unexpected home repair last year. They have $2,256 on a high-interest credit card and $15,000 on a line of credit. They want to pay off this debt as quickly as possible. They make a total of $800 in monthly payments, $300 towards the credit card and $500 towards the line of credit. In the plan, we help Michael and Julie make a monthly debt payoff plan and pay their debt off faster.

Income Planning

Over the next few years Michael and Julie’s income will fluctuate as they take time off from work to care for their new baby. Employment income will drop but this will be partially offset with employment insurance benefits. When it comes to retirement Michael and Julie will have 10 different income sources to plan for. We’ve planned retirement withdrawals to help minimize tax and maximize benefits.

Spending Projections

With new baby, Michael and Julie will see their spending increase over the next few years. With day care and new expenses their household spending will increase from $47,484 and peak at $64,748 before dropping back down again. To avoid debt in the future we’ve planned for $445/month for infrequent expenses. In retirement, we’ve planned for an increase in travel expenses which will slowly decrease as Michael and Julie get older.

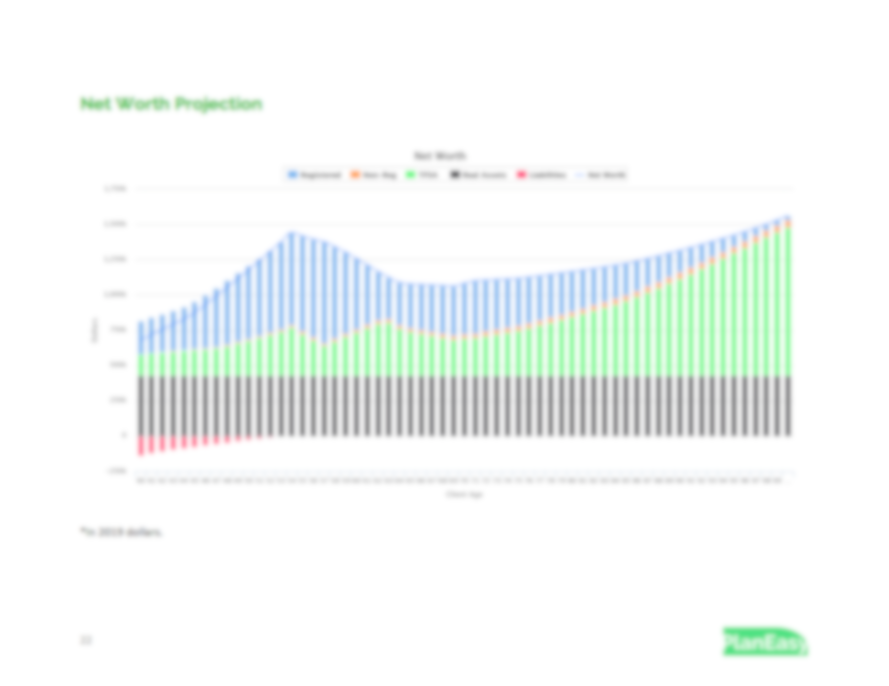

Net Worth Projections

With a low-cost investment portfolio Michael and Julie will see their net worth grow considerably. Even with fluctuations in income and expenses they will still able to save a small amount each month. These savings are initially directed toward RRSP to optimize their tax and benefits. In retirement, we slowly shift registered investments into TFSA to help minimize tax on their estate and increase flexibility.

Gov. Benefits, CPP, and OAS

Because Michael and Julie want to plan for retirement at age 55 they cannot expect to receive full CPP benefits. We calculate what they can expect from retirement benefits like CPP and OAS based on contributions and time in Canada. We also calculate other government benefits like GST/HST credit, Canada Child Benefit (CCB) and provincial benefits. These benefits add over $120,000 to Michael and Julie’s plan.

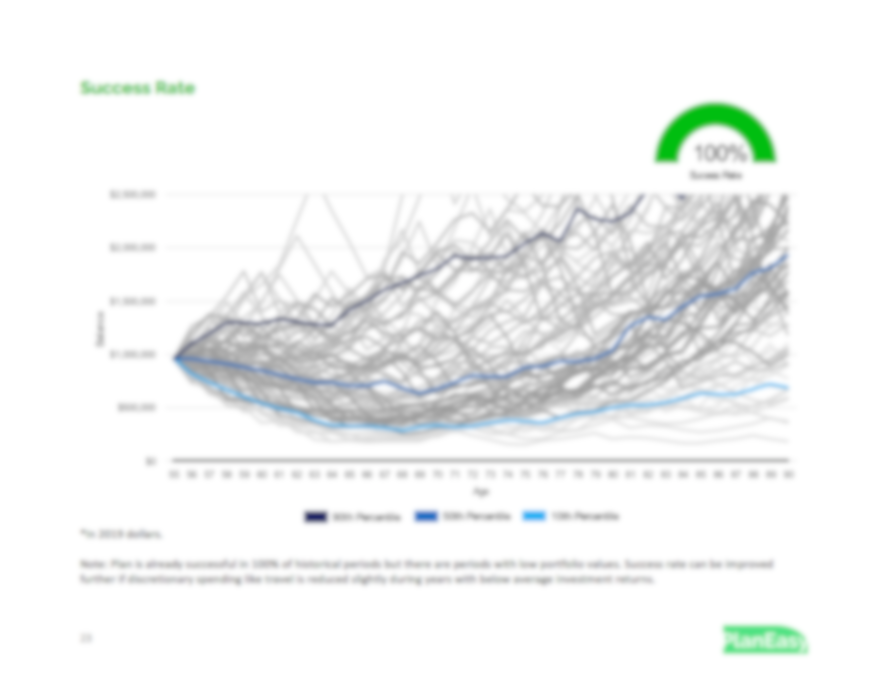

Security & Peace of Mind

For health reasons Michael and Julie want to plan for early retirement at age 55. If they can, they may choose to work longer, but they want to have the flexibility to retire at age 55 if they choose. To ensure their plan is successful regardless of what happens in the future we tested their plan over multiple historical scenarios. Michael and Julie can feel secure knowing that their plan is successful even during the worst periods of historical stock/bond/inflation rates.