Managing Cash Flow Using

The Digital Envelope Budget System

Whether it’s a torrent or a trickle, having a system to manage cash flow can help make money easy. One of the most time-consuming things about personal finances is managing income and spending. But what if you had a budgeting system that helped you manage that monthly cash flow? And what if that system was free, easy to set up, and simple to maintain?

Managing income and spending is the best way to achieve financial freedom. It doesn’t take much to go from financial ruin to financial success. It can be as little as $10 per day. It’s not about stellar investment returns, or risky real estate investing, or earning six figure salary, it’s all about paying attention to income and spending.

But old methods of managing cash flow need to be updated for the digital age. Cash is less prevalent, and credit and debit transactions dominate. Any system for managing income and spending needs to be digital, automated, and easy to set up and maintain.

The envelope budget is a classic way to manage income and spending. It’s a proven way to manage cash flow and it’s easy to understand. Money gets allocated to certain envelopes and spent during the month. As money in an envelope gets low this provides a signal to slow down on spending until the envelope gets replenished on the next payday.

Thanks to no-fee online bank accounts, the envelope budget can be easily adapted to the digital age.

But it’s not as simple as just creating a few new bank accounts. To manage cash flow with the digital envelope budget system it helps if you have a budget already created. This may require tracking your spending for a few weeks or months. Or it may require looking at past statements. It also requires an online no-fee bank account.

This is how you set up the digital envelope budget system.

Start With A Budget

To create a system to help manage income and spending it helps if you have a budget already created. Without knowing where your money is currently going it can be tough to create a system that really works. To use the digital envelope budget system you need to know how much money to put in each envelope. This starts with a rough budget.

Creating a budget may require tracking your spending for a few weeks or months. Or perhaps looking at past credit card and bank statements. By looking at actual purchases the budget will be more realistic and easier to manage. The best budgets are based on reality.

Once you have your actual spending/budget you can move onto the next step.

Setting Up The Digital Envelope Budget System

In the past, the envelope method would consist of multiple envelopes with cash in them. Each envelope would have cash that was allocated for a specific purpose, food/groceries, restaurants, clothing, rent, utilities, savings etc.

Each envelope would get replenished with new cash on payday and would have cash removed as purchases were made.

Money goes in, money comes out. When there’s no money left in an envelope, or money is getting low, then it’s time to slow down on spending until the next payday.

To do this digitally we need a few ‘virtual’ envelopes. Luckily, no-fee online bank accounts are perfect for this. We personally use Simplii and Tangerine for this. Money comes in on payday and then gets allocated to our various accounts.

For couples you may also have a joint account set up for shared household expenses like rent, mortgage, utilities etc. We’ve had a joint account set up since before we were married. Some of our regular income gets funneled into the joint account to cover shared household spending.

We particularly like Tangerine for our digital envelopes because you can set up multiple savings accounts and name them individually. Between Sue and I we have over a dozen accounts to help manage our personal spending. This seems like a lot but they’re all summarized nicely in each app.

Start With The (Cash) Flow

It’s best to sketch out your “flow” on paper before setting up the individual accounts and automated transfers.

Start with money coming in, this is typically net income from an employer. How much is it? How often do you get paid? Is it weekly, bi-weekly, semi-monthly, monthly etc. For parents or lower income earners, income may also need to include income from government benefits like the Canada Child Benefit.

Next is money coming out. What are the envelopes you want to use? What are they for? The best envelopes won’t be too specific. For example, you may lump all personal spending into one envelope. This reflects the reality that specific spending categories may be higher or lower than budget in a given month. For example, you may spend more on clothing and less on restaurants one month. As long at the total is on track that’s the main goal.

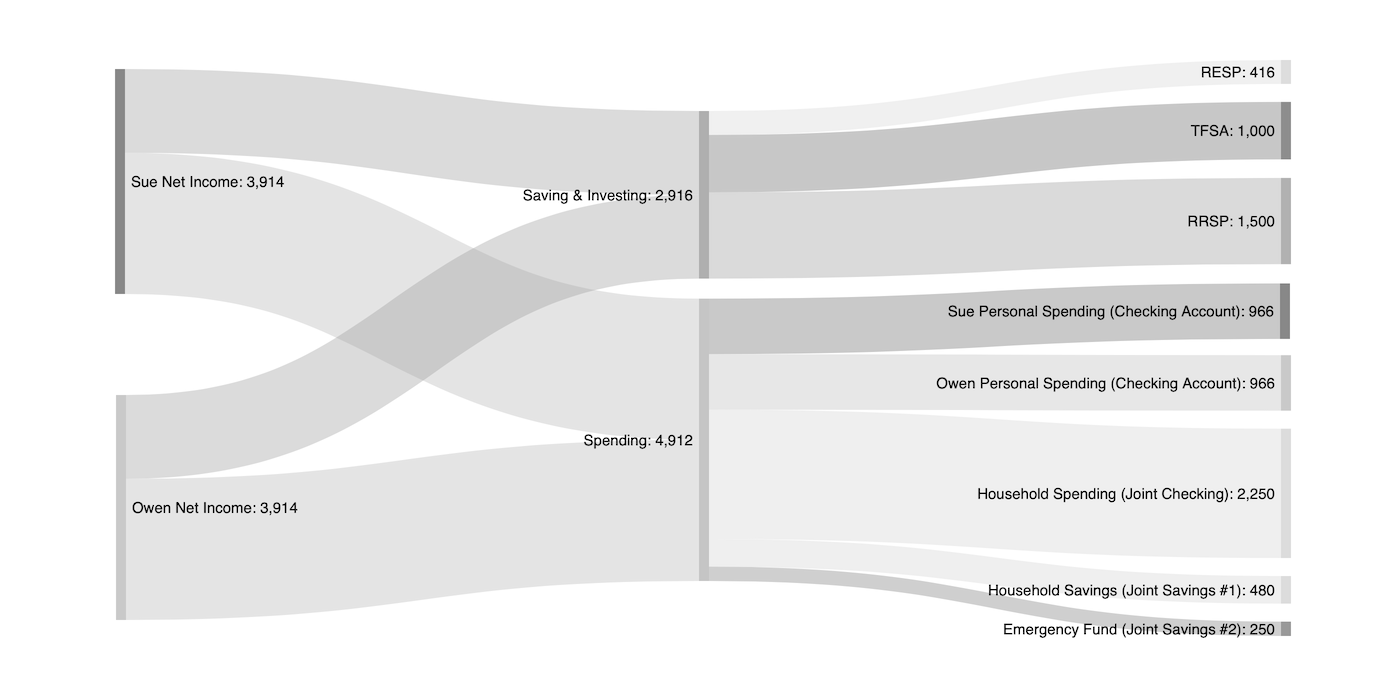

We personally use the following envelopes. Personal spending x 2, household spending, household savings (infrequent expenses like home repairs, vehicle upgrades, vehicle repairs etc), and emergency fund. We also put money into investments each month, both for RESP and retirement.

Here’s what our flow looks like (the numbers are made up). We even use additional envelopes in our personal accounts that I’ve left out of this flow. For example, we plan ‘gift’ money on a monthly basis, so I have a personal savings account that holds the excess, this gets drawn down as I purchase gifts and slowly replenished each month.

Free Resources

Setting Up The Automated Transfers

The last thing is to set up the automated transfers. This is where the digital envelope budget truly shines. These automatic transfers can be set up to align with your pay cycle. The day after pay day you can have money funnel into each account automatically. This “set it and forget it” automation makes the digital envelope method really powerful.

The nice thing about automated transfers is that it doesn’t require any ongoing maintenance. You may update the amounts every few months but only if spending changes (maybe daycare expenses end!).

This automation also is powerful because once the money is out of sight, it’s also out of mind. By using the digital envelope budget system, you will quickly adapt to a new level of spending.

We choose to leave personal spending in our checking account and it gets replenished with each paycheck. This always gives us a good sense of how much we have left to spend before next payday (and allows us to adjust our spending accordingly). Because we see both our credit card and checking account in the same app/screen its easy to see how much we have left to spend each month. We never go over our monthly budget because once the money is gone, it’s gone.

Managing Cash Flow Made Easy

Having a system to manage cash flow can help make money easy. Managing income and spending is the best way to achieve financial freedom over the long run. Saving and investing a little bit each month is all it takes.

Using the digital envelope budget method is one way to manage cash flow. It’s easy, automated, and can be completely customized. It’s easy to set up and simple to maintain.

When aligned with your pay cycle the automated transfers money between digital envelopes. It will whisk money away without you even noticing. It’s out of sight and out of mind.

The digital envelope method is probably one of the best ways to manage money there is. As budget it’s detailed enough to help manage your money, but not too detailed to become onerous and overwhelming. It’s the perfect mix of practical and effective.

Join over 250,000 people reading PlanEasy.ca each year. New blog posts weekly!

Tax planning, benefit optimization, budgeting, family planning, retirement planning and more...

Join over 250,000 people reading PlanEasy.ca each year. New blog posts weekly!

Tax planning, benefit optimization, budgeting, family planning, retirement planning and more...

0 Comments