by Owen | May 5, 2025 | Retirement Planning

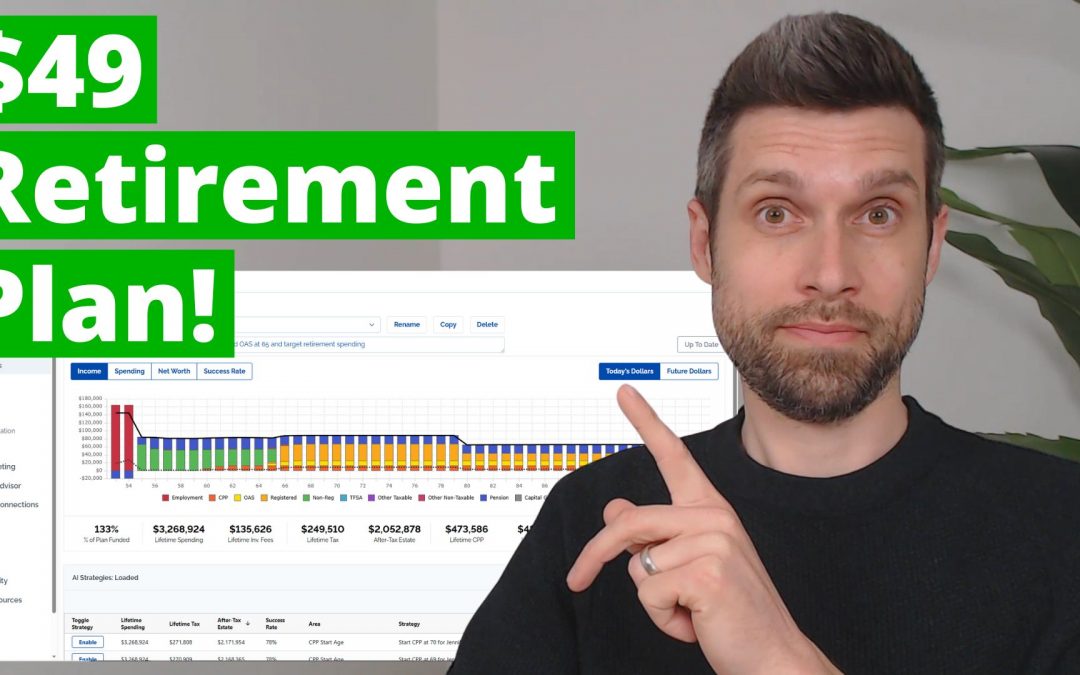

We’re excited to introduce the $49 Retirement Plan. This is an exciting new way to create a retirement plan in Canada!

With PlanEasy our goal from the very beginning was to make retirement planning easy, accessible, and inexpensive.

With this new $49 Retirement Plan from our sister company Adviice we are getting extremely close to that goal.

What is Included in the $49 Retirement Plan?

When you sign up for the $49 Retirement Plan, you’re getting more than just the software platform, you’re getting access to a full retirement planning ecosystem built to provide you with clarity, confidence, and control over your financial future.

You’re getting access to…

– Retirement Planning Platform

– AI Strategies

– Community Support Forum

– Educational Webinars (2x per Month)

– Optional 1:1 Platform Training

by Owen | Jan 1, 2025 | Financial Goals, Financial Planning, Government Programs, Retirement Planning

Did you know that the Canada Pension Plan (CPP) is getting bigger? Every year since 2019 CPP has been expanding and it will continue to expand for the next 40+ years until 2065. By the end, CPP will be HUGE!

CPP is an important retirement benefit. The old “base” CPP aimed to replace 25% of pre-retirement employment income. The new “expanded” CPP will increase this amount to 33.33% and will cover a larger amount of pre-retirement of income. The result is that CPP will be over 50% larger in the future.

If we follow the rule of thumb* that suggests that we need 70% of pre-retirement income in retirement, then for the average Canadian the new expanded CPP could provide nearly half of retirement income in the future. When combined with OAS this means that over half of retirement income could be covered by CPP and OAS combined.

And if we consider that the maximum annual CPP payment could be over $7,000 per year higher in the future (and over $14,000 per year for a couple), that could mean the average Canadian needs to save hundreds of thousands less for retirement.

In this post we’ll look at the current maximum CPP payment, the maximum CPP contribution, the current contribution rate, and how these will change in the future as CPP expands. We’ll also look at how the current “base” CPP will grow by over 50% in the future…

by Owen | Dec 11, 2023 | Government Programs, Income, Investment Planning, Retirement Planning, Tax Planning

A solid retirement plan can help unlock hidden opportunities and it can help make retirement easier and more enjoyable. In this blog post we’re going to explore a retirement planning case study with only $250,000 in financial assets at retirement.

We’re going to help them maximize government benefits, minimize taxes, and increase spending in retirement.

To do this we’re going to use a few different retirement planning strategies…

Retirement Spending Phases

– RRSP Meltdown

– GIS Maximization

– Strategic RRSP Contributions 65-71

– Strategic RRSP Withdrawal At 72

– CPP & OAS Timing

Don’t forget to watch the video where we build this retirement plan in real time. If you enjoy this case study and would like us to do a case study based on your situation, then please leave a comment.

by Owen | Jun 11, 2023 | Financial Planning, Investment Planning, Retirement Planning

There are a lot of risks that we face in retirement. When you enter retirement, there are lots of changes happening all at once. Along with big personal changes, and lifestyle changes, there are also big changes happening to your finances. After you enter retirement one of the biggest financial changes you’ll face is a shift from a regular income source (eg. employment) to an income source based entirely on your own savings and pension. Making this switch can create a few risks, one of those risks is the risk of running out of money.

One of the biggest risks facing retirees is something called sequence of returns risk. When a good portion of your retirement income comes from your own savings this is the biggest risk a retiree can face. But what does “sequence of returns risk” mean exactly?

Before we talk about sequence of returns risk it’s important to understand that most retirement plans are based on an assumed (and constant) investment return each year. This investment return is usually assumed to happen in a straight line with the same percentage return each year. An assumed return of return of 5% would be 5% per year starting on the day you retire, but in reality your investment return is going to fluctuate from year to year, and this is where the risk comes from.

Over the short-term you will probably see your investment return fluctuate greatly from year to year. Instead of seeing investment returns of +5%, +5%, +5%, +5%, +5%, you might see +20%, +2%, -10%, +15%, +1%. In this case the average return is still +5%, but there were some huge swings from year to year. “Sequence of returns risk” refers to this sequence, the actual investment returns you see year after year.

The big risk for retirees happens when the sequence is negative for a few years in a row. Even if average investment returns recover over the long-term, that short period of negative returns can have a devastating effect on a retiree’s portfolio.

by Owen | May 29, 2023 | Financial Planning, Investment Planning, Retirement Planning, Tax Planning

When to convert RRSP to RRIF? What is the right time to convert? What are the advantages of converting?

Converting an RRSP to a RRIF is mandatory by the end of the year you turn age 71. This triggers mandatory minimum withdrawals the following year and each year after that. The minimum withdrawal is based on the ending balance the previous year and the account holder’s age.

There is a common misconception that you should wait until the last possible moment to convert an RRSP to a RRIF. Maybe this is because it’s a “forced” conversion? Something that’s forced couldn’t be good right? Perhaps it’s because RRSPs grow tax free? Why not delay withdrawals as long as possible, why voluntarily make withdrawals by converting to a RRIF early?

Despite the misconceptions above, in many cases, converting an RRSP to a RRIF should be done much earlier than age 71.

There are many reasons for a retiree to convert an RRSP to a RRIF well before the mandatory age of 71. In this post we’ll highlight some of the considerations when deciding when to convert RRSP to RRIF.

by Owen | Apr 24, 2023 | Behavioral Finance, Buying A Home, Financial Planning, Government Programs, Investment Planning, Retirement Planning, Tax Planning

The largest financial transaction you will ever make is selling your home in retirement. Selling your home in retirement comes with a number of important considerations.

In this blog post we’re going to touch on 9 important things to consider when selling your home in retirement.

Selling a home in retirement can be a core part of many retirement plans. A sale usually takes one of three forms…

– Sell and rent

– Sell and downsize

– Sell when entering long-term care

Often the plan is to hold the home throughout retirement, but it can still be used as a “fall back” asset if necessary. Even if there was never a plan to sell the home, it can still be used to help fund long-term care costs in late retirement.

Each situation above has its unique circumstances but, in all cases, there is a major transaction taking place. So, before you put up the ‘for sale’ sign in retirement there are a few important considerations to highlight.